Your Personal Allowance is one of the biggest tax planning opportunities for UK seafarers. One of the biggest financial advantages of working at sea is the potential to qualify for the Seafarers’ Earnings Deduction (SED), which can mean your seafaring income is free from UK income tax.

Because of this, a lot of crew stop thinking about tax planning altogether, but there’s a key opportunity that is often overlooked: your personal allowance.

For many seafarers, this allowance largely goes unused every year, even though it can be used to generate additional tax-free income.

What your Personal Allowance means for you

Your personal allowance is the amount of net income you can earn each year, before you start paying income tax.

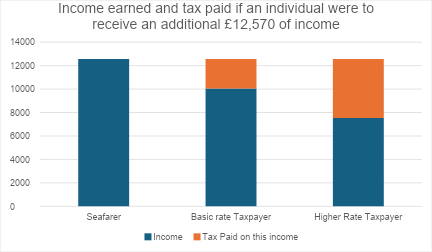

The standard personal allowance is currently £12,570.

For most yacht crew, this allowance isn’t used at all because their seafaring income is already covered by the SED.

In simple terms, this means you are able to earn additional income up to the value of your personal allowance without paying UK income tax.

Once your income exceeds the £12,570 threshold, you will start paying income tax of 20% on this excess amount, until you reach the next tax threshold (£50,270).

*- infographic example below but could use improving

Sources of additional Tax-Free Income

There are several ways crew members may choose to make use of their personal allowance while their main income remains tax efficient.

Examples include:

- Rental Property income from a rental property in the UK

- This is calculated from rental profits (gross rental income less applicable rental expenses)

- Land based work:

- Some examples of this could include:

- Freelance painting and varnishing

- Carpentry work

- Freelance cleaning

- On-demand IT services

- Zero-hour contracts – for example, bartending or service work

- As a Uk tax resident, any land-based income will be subject to income tax, even if this work was undertaken outside the UK

- Some examples of this could include:

- Dividend incomefrom non-ISA investments:

- We recommend maximising your ISA investments before investing via a general investing account. However, if you have maximised your ISA and are still investing then dividends earned from this will use up your personal allowance.

- The first £500 of dividends is always tax free.

- Interest income from savings accounts:

- Interest income from savings also has a few separate allowances:

- £5000 starter rate of 0% if your other income (not including seafaring income) is below 17,570.

- The £5,00 starter rate does decreases by £1 for every £1 your other income exceeds £12,570.

- £1,000 personal savings allowance if you are a basic rate taxpayer or £500 if you’re a higher rate taxpayer.

- Commissions and referrals:

- Commission – Earning income from selling goods or services

- Referral fees – Certain companies will pay you if you refer a client to them, such as our sister company Superyacht Tenders (SYT)

Because many crew rely on a single income source, these types of income streams can help diversify finances without creating a tax bill.

It’s important to note that the sale of assets (property, non-ISA stocks and shares, cryptocurrency, etc) falls under Capital Gains Tax which is entirely separate to income tax and your personal allowance.

Making the most of your personal Allowance:

Working at sea gives many seafarers a unique financial position compared to most UK taxpayers. With the right approach, you can:

- Keep your seafaring income tax-efficient

- Generate additional income without creating a tax liability

- Build savings and investments more effectively

For more assistance with maximising your personal allowance, contact CrewFO via:

Email at: hello@crewfo.com

Phone call through: https://calendly.com/hello-crewfo/crewfocall